Paradox in Economic Headwinds: Recession or Inflation

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

If Recession, Then Not Inflation

Last week, I wrote about the Fed Funds Futures curve, concluding rate cuts will likely start in the middle of next year, giving bitcoin plenty of room to rally through the halving season. That analysis is based on the high probability that a recession is coming, which does not match with the common belief that inflation is heating back up. Today, I want to discuss a couple common paradoxes to clear up that disconnect.

US 10-Year Treasury is Blowing Up

The rise in the US 10-year Treasury yield has been awe-inspiring, breaking to 16-year highs. To many people, this is a harbinger of a monetary doomsday feedback loop.

Higher yields mean higher interest payments for the government, a weaker economy, higher inflation, more money printing, and even higher yields. The key ingredient of that feedback loop is more money printing. If the economy can increase the money supply, a recession will be avoided, but will instead trade-off for higher inflation and yields. Without an increase in private credit creation, the feedback loop collapses in on itself and moves toward recession and deflation.

Here we have our first widely-believed paradox, that we can be heading into a severe recession and going to suffer an inflationary doom loop at the same time. In reality, these are mutually exclusive outcomes in the modern economy.

Yields fall in recessions and deflation becomes the primary concern, especially in the post-Great Financial Crisis (GFC) era where the increased debt burden outweighs the productivity of new debt. Either we are headed for recession or yields and inflation are going to run hot.

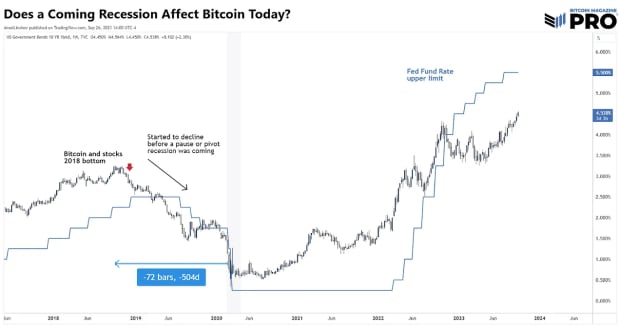

It is hard to find someone who doesn’t see major signs of recession. People are tapped out and most analysts see the elusive soft-landing as a best case scenario. Recession is a pretty safe bet. Therefore, we have to expect rates to peak soon and start coming down. We cannot be sure when, but before the Fed pivots or an official recession is declared.

Above, the 10Y peaked in 2018, long before a rate cut from the Fed or a declared recession. Either private credit creation rises dramatically to support higher yields and CPI or market yields will turn, leading the Fed’s policy lower into recession.

Oil and Inflation

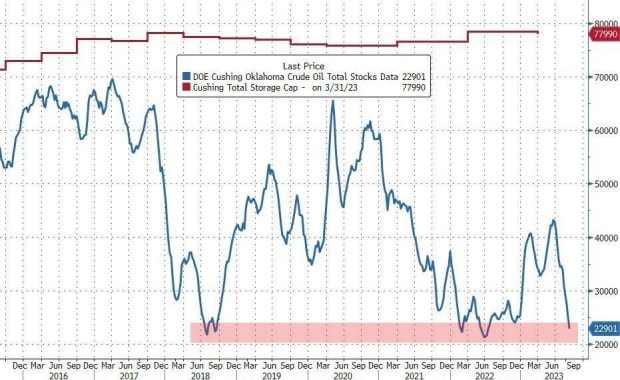

Many cite the cost-push effect of the rising oil price as a cause for inflation to re-accelerate. This morning, I saw this chart in an article from Zerohedge, “Oil Can Push Higher As Cushing Stockpiles Collapse,” and it beautifully exemplifies the prevailing confusion. Do inventory levels at Cushing, OK matter at all to the price of oil?

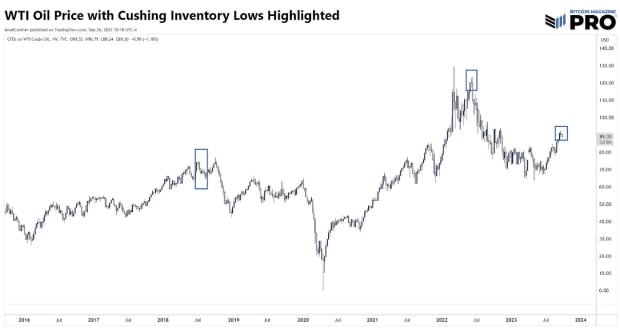

Above, I lined up WTI oil futures for the same period as the Cushing inventory chart and highlighted the prices at the LOWS in inventory: July 2018, June 2022, and today. Would you say those are at tops or bottoms?

This is our second paradox of the day, rising oil prices can cause recessions and inflation at the same time in our modern economy. In reality, it is not a causal relationship. Low inventory levels do not equal tight supply. Both inventory levels and price are symptoms of more basic supply and demand in the real economy.

Low inventories and high oil prices mean demand has been outstripping supply. Those high oil prices, in turn, cause demand destruction forcing demand to fall, allowing prices to fall and inventory to build. This is very clear on the chart and is the dominant dynamic unless it is met with increased levels of private credit creation.

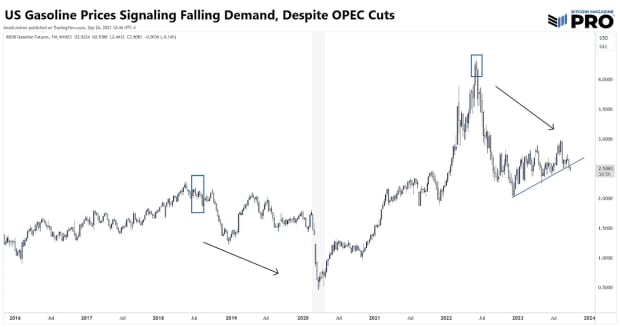

Gasoline futures are also breaking lower. Again, I highlight the Cushing lows which are followed immediately by falling prices. The exact opposite of the prevailing wisdom. Does this look like cost-push inflation from oil is headed our way? No, it looks like demand is declining into recession.

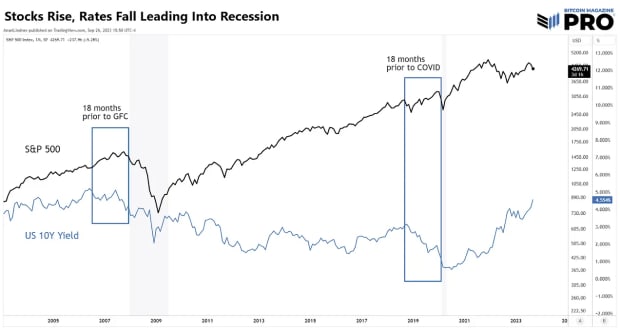

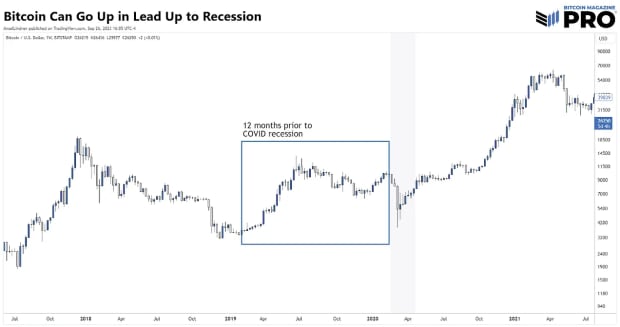

US Stocks and Bitcoin

To round out today’s coverage, let’s take a look at stocks and Bitcoin. It is true, during an official recession stocks typically go down. However, the year leading up to a recession is usually bullish. Bitcoin has only experienced one recession, but right now, we expect it to behave like risk assets.

Our forecast is for an approaching recession starting in the second half of 2024 or even later. That would mean this current sell-off in stocks (that happens to be corresponding with the seasonal crunch at the end of Q3), and lackadaisical performance of bitcoin, have a year to reverse and rally.

This is the final paradox of the day, an approaching recession is good for risk assets. The year leading into recessions are characterized by falling Treasury yields, falling economic demand, and hence falling CPI. That is why so many PhD economists at the Fed are tricked into not seeing the recession coming.

This is positive for stocks and bitcoin because of asset price inflation, or the rise in the price of assets coupled with a stagnant economy. In the lead-up to recession, lenders become weary of the economy and narrow access to credit. As credit tightens into recession, rates fall and only the most creditworthy and trusted borrowers maintain access to new credit. The largest stocks will benefit, while Mom-and-Pop businesses are starved for credit.

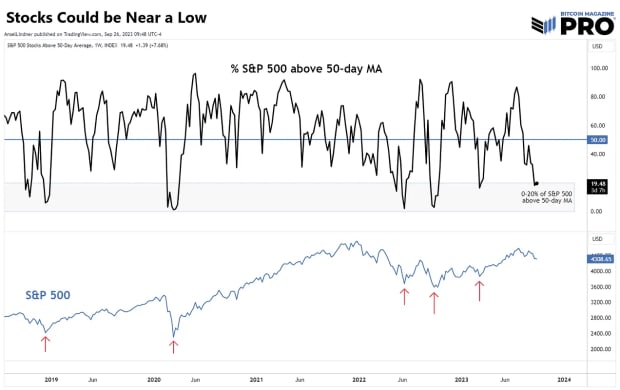

If recession is approaching, we should therefore expect stocks and bitcoin to rise in the medium term, only to fall when recession is imminent. A near-term reversal in stocks is supported by the percent of S&P 500 stocks above their 50-day moving averages. When it is below 20%, it corresponds to bottoms.

Summary

A recession is coming which precludes higher for longer CPI inflation and yields. However, it is still a long way off and in the interim, we should expect stocks and bitcoin to rise as yields, oil and CPI decline.

4 October 2023 15:00