What is hyperinflation and how does it happen?

“Gradually, then suddenly,” goes the Hemingway trope about going bankrupt that Bitcoiners have so enthusiastically adopted. When crypto exchanges, stablecoins and banks are collapsing left and right, it looks suspiciously like we are already in the “suddenly” portion. And it is suddenly that currencies of the past have moved from the pocketbooks to the history books.

Hyperinflation is a general increase in prices by 50% or more in a single month. Alternatively, sometimes economists and journalists use a lower rate of monthly inflation sustained over a year (but that still amounts to 100%, 500% or 1,000%). The imprecision leads to some confusion in what does or does not constitute a hyperinflation.

Definitional quibbles aside, the main point is to illustrate the ultimate death of a fiat currency. Hyperinflation of whichever caliber is a situation where money holders rush for the exits, like depositors in a bank run rush for their funds. Literally anything is better to hold on to than the melting ice cube that is a hyperinflating currency.

A hyperinflating currency is often accompanied by collapsing economies, lawlessness and widespread poverty; and is usually preceded by extremely large money printing in service of covering equally vast government deficits. Double- or triple-digit increases in general prices cannot happen without a massive expansion of the money supply; and that generally doesn’t take place unless a country’s fiscal authority has difficulty financing itself and leans on the monetary authority to run the printing presses.

BACKGROUND: What Hyperinflation is and how it happens

In 1956, the economist Phillip Cagan wanted to study extreme cases of monetary dysfunction. As we’ve learned over the past few years, whenever prices go berserk there is a big kerfuffle about who’s to blame — greedy capitalists, vague supply chain bottlenecks, unprecedented money printing by the Fed and fiscal deficits by the Treasury or that evil-looking dictator halfway around the world.

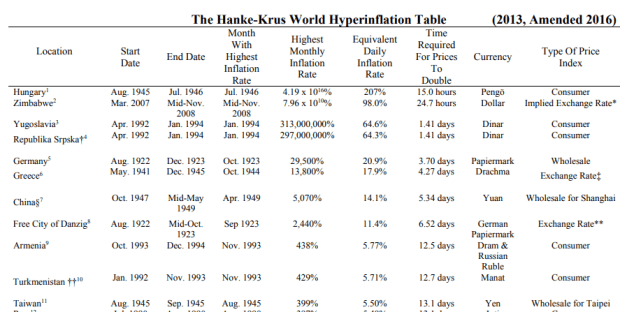

Cagan wanted to abstract away from any changes in “real” incomes and prices, and therefore placed his threshold at 50% price rises in a single month; any offsetting or competing changes in real factors, said Cagan, can then be safely disregarded. The threshold stuck, even though 50% a month makes for astronomically high rates of inflation (equal to about 13,000% annually). The good news is that such an extreme collapse and mismanagement of fiat money is rare — so rare, in fact, that the Hanke-Krus World Hyperinflation Table, often considered the official list of all documented hyperinflation, contains “only” 57 entries. (Updated for the last few years, its authors now claim 62.)

The bad news is that inflation rates well below that very demanding threshold have destroyed many more societies and wreaked just as much havoc in their economic lives. Inflation “bites” at much, much lower rates than that required for going into “hyper.”

Nobody does inflation like us moderns. Even the most disastrous monetary collapses in centuries past have been rather mild compared to the inflations and hyperinflations of the fiat age.

What Hyperinflation Looks like

“Hyperinflation very rarely occurs all of a sudden, without any early warning signs,” writes He Liping in his Hyperinflation: A World History. Rather, they stem from earlier episodes of high inflation that escalate into the hyper variety.

But it’s not particularly predictive, since most episodes of high inflation do not descend into hyperinflation. So what causes general periods of high inflation in the tens or twenties of percent that most Western countries experienced in the aftermath of Covid-19 pandemic in 2021-22 is different from what causes some of those episodes to devolve into hyperinflation.

The list of culprits for high inflation regimes include

- Extreme supply shocks that cause prices of key commodities to rise rapidly for a sustained time.

- Expansionary monetary policy that a) involves central bank printing a lot of new money, and/or b) commercial banks lending freely, without restraint.

- Fiscal authorities run fiscal deficits and ensure that aggregate demand runs hot (above trend or above the economy’s capacity).

For high inflations to turn into hyperinflations, more extreme events must take place. Usually, the nation-state itself is at risk such as during or after wars, a dominant national industry collapses or the public loses trust in the government entirely. More extreme versions of the above are usually involve

- A fiscal authority running extremely large deficits in response to nation-wide or dependent industry shocks (pandemics, war, systemic bank failures).

- The debt is monetized by the central bank and forced upon the population, often through the use of laws that mandate payments in the nation’s currency or bans the use of foreign currencies.

- Complete institutional decay; efforts to stabilize the money supply or the fiscal deficits fail.

In a hyperinflation event, holding cash or cash balances becomes the most irrational of economic actions, yet the one thing a government needs its citizens to do.

There is only so much printing you can — or would — do if there weren’t underlying problems or fiscal authorities breathing down your neck; there are only so much additional money the public wishes to hold, and when you start up the presses, the seigniorage profit you can extract becomes smaller and smaller when they ditch your currency for literally anything else. (“People are exchanging their dollars for dog money.”)

Everybody wants to transact, often trying to get their wages paid several times a day and head to the store to purchase anything. Everybody wants to borrow or consume on credit — since one’s debt will disappear in real terms — yet nobody wants to lend: banks usually curtail lending, and credit runs dry. Prior debts are completely wiped out, as they were fixed in nominal terms. A hyperinflation event closely resembles a “clean slate,” a way for collapsed nation-states to restart, monetarily speaking. They reshuffle the net ownership of hard assets like property, machinery, precious metals or foreign currency. Nothing of financial consequence remains: all credit ties are inflated into nothingness. Financial ties no longer exist. It’s the ultimate weapon of mass financial destruction.

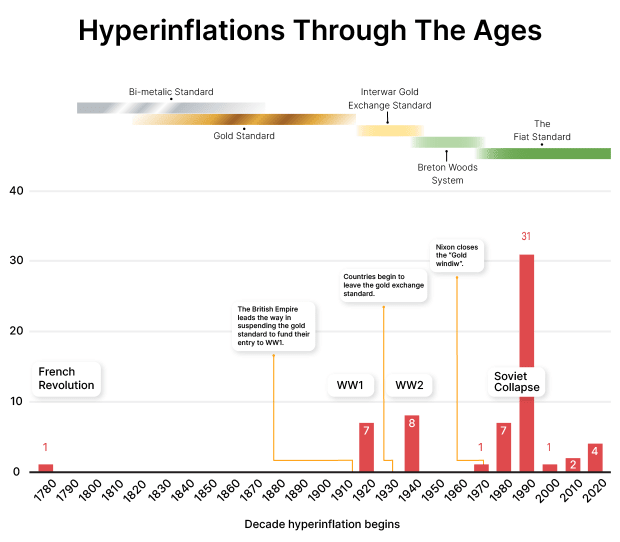

History of hyperinflations

Though the first cited instance is usually revolutionary France, the modern times contain four clusters of hyperinflations. First, the 1920s when the losers of WWI printed away their debts and wartime reparations. This is where we get the wheelbarrow imagery and which Adam Fergusson’s classic When Money Dies so expertly chronicles.

Second, after the end of World War II, we have another bout of war-related regime collapses leading rulers to print away their unsustainable obligations — Greece, Philippines, Hungary, China, and Taiwan.

Third, around the year 1990 when the Soviet sphere of influence imploded, the Russian ruble as well as several Central Asian and Eastern European countries saw their defunct currencies inflate away into nothingness. Soviet-connected Angola followed suit, and, in the years before Argentina, Brazil, Peru and Peru again.

Fourth, the more recent economic basket cases of Zimbabwe, Venezuela and Lebanon. They all present stories of obscene mismanagement and state failure that while not exactly mirroring the previous clusters of hyperinflations, at least share their core features.

Egypt, Turkey and Sri Lanka are other nations whose currency debasements in 2022 were so stunningly bad as to merit a dishonorable mention. Though disastrous for these countries’ economies and tragic for the holders of their currencies — with head-spinning high inflation rates of 80% (Turkey), 50%-ish (Sri Lanka) or over 100% (Argentina) — it is scant relief that their runaway monetary systems are long ways off to formally qualify as hyperinflations. You get terrible outcomes way before runaway inflation crosses the “hyper” threshold.

High inflation episodes (double digits or more) are not stable. The printing by authorities and monetary flight by users either accelerate or slow down; there is no such thing as a “stable” 20% inflation year after year.

What’s clear from the historical record is that hyperinflations “are a modern phenomenon related to the need to print paper money to finance large fiscal deficits caused by wars, revolutions, the end of empires, and the establishment of new states.”

They end in two ways:

- Money becomes so worthless and dysfunctional that all its users have moved to another currency. Even viable governments that keep forcing their hyperinflating currencies onto the citizenry through legal tender and public receivability laws, receive only minor benefits from printing. Currency holders have left for harder monies or foreign cash; there is precious little seigniorage left to extract. Example: Zimbabwe 2007-2008, or Venezuela 2017-18.

- Hyperinflation ends by fiscal and monetary reform of some sort. A new currency, often new rulers or constitution, as well as support from international organizations. In some cases, rulers seeing the writing on the wall purposefully hyperinflate their collapsing currency while preparing to jump to a new, stable one. Example: Brazil in the 1990s or Hungary in the 1940s.

While currency collapses are a most painful reminder of monetary excesses, their ultimate causes are almost always fiscal problems and political disarray — a chronic weakness, a flailing dominant industry, a runaway fiscal spending regime.

The three basic functions of money — medium of exchange, unit of account, store of value — are impacted differently by instances of very high inflation or hyperinflation. Store of value is the first to go, as evidenced by pictures of wheelbarrow inflation; the money becomes too unusable a vehicle through which to move value across time. The unit of account role seems remarkably resilient in that money users can change price tags and adjust mental models to the ever-shifting nominal prices. Accounts from Zimbabwe, Lebanon or South America indicate that money users can keep “thinking” in a currency unit (keep performing economic calculation) even though the rapid changes in daily value makes it harder to do this well.

Both hyperinflation and high inflation are severe headwinds on economic output and a wasteful use of human efforts, but money’s “metric role” doesn’t immediately go away. The medium of exchange role, which economists have long held to be the foundational monetary role from which the other functions stem, seems to be the most resilient. You can transact, hot potato-style, even with hyperinflating money.

Read More >> What is Money?

What happens: The few winners and many losers

The natural reaction of Germans and Austrians and Hungarians, wrote Adam Fergusson in his classic account of the hyperinflations in the 1920s When Money Dies, was “to assume not so much that their money was falling in value as that the goods which it bought were becoming more expensive in absolute terms.” When prices rose, “people demanded not a stable purchasing power for the marks they had, but more marks to buy what they needed.”

Hundred years later — a different time in different lands with a different money — the same doubts go through people’s minds. Inflation, of its hyper-variety or the ones we’re living through in the 2020s, muddies people’s ability to make economic decisions. It gets harder to know how much something “costs,” if a business is making a real profit or if a household is adding to or depleting its savings.

The Economist’s account of the effects of Turkey’s inflation last year summarized the economy-wide consequences of inflation running amok. Under high (or hyper-)inflation, time horizons shrink and decision-making collapses to day-to-day cash management. Like all inflations there are arbitrary redistributions of wealth:

- The economic cost of high inflation is the unpredictability of the price system, the volatility of prices themselves. If you think bitcoin’s exchange rate to the USD is “volatile,” you haven’t seen basic prices in hyperinflating countries — wages, assets, grocery stores, rents. It undermines consumers’ ability to plan or make economic choices. Production gets delayed, investment decisions postponed and the economy squeezed since spending decisions are brought forward to the present.

- In a similar vein, price signals don’t work as well anymore. It’s harder to see through the nominal prices to the real economic factors of supply and demand — like the car window into the economy suddenly becoming foggy. Haggling over exact prices makes transaction costs shoot up, which benefit nobody; partially substituting the failing money for foreign currency adds a second layer of (often black-market) exchange rates to juggle.

- It’s unfair. Those best placed to play the inflation game, to shelter their wealth through property, hard assets or foreign currencies, can protect themselves. It causes a rift between those who can access foreign currency or hard assets, and those who cannot.

While most people’s economic lives are disrupted by (hyper)inflation and in aggregate everyone loses, some people benefit along the way.

- The most obvious losers are those holding cash or cash balances, since these are straight away worth less.

- The most direct beneficiaries are debtors, whose debt gets inflated away; insofar as they can have their incomes keep pace with the fast rises in prices, the real financial burden of the debt disappears. The flipside of that is the creditor, who loses purchasing power when their fixed-value asset deflates into nothingness.

Do governments benefit from high or hyperinflation?

There is a lot of nuance to whether governments benefit from high inflation. The government itself usually benefits, since seigniorage accrues to the issuer of the currency. But general tax collection doesn’t happen instantly and so taxes on past incomes may be paid later in less valuable, inflated money. Besides, a poorer real economy usually makes for less economic resources that a government can tax.

Another way governments benefit is that their expenses are usually capped in nominal terms while tax receipts rise in proportion to prices and incomes.

As a large debtor, a government all else equal, has an easier time nominally servicing its debt — indeed, large government debts and financial obligations are major reasons to hyperinflate the currency in the first place. On the other hand, international creditors quickly catch on and refuse to lend to a hyperinflating government, or demand that they borrow in foreign currency and at additional interest rates.

Some institutional features matter too. To take two recent examples from the U.S.: Social Security indexation and the loss of income from the Fed. While the debt that gets inflated away involves a government’s pension obligation to retirees, there may be indexed compensation when prices rise. In December 2022, Social Security payments were adjusted upwards by 8.7% to account for the inflation captured in CPI over the last year. In more extreme cases of inflation or hyperinflation, such compensation might be delayed, or less stable governmental institutions may lack such features altogether, which would result in cuts in financial welfare for the elderly.

Similarly, when the Fed hiked rates aggressively during 2022, it exposed itself to accounting losses. For the foreseeable future it has therefore suspended its $100 billion in annual remittances to the Treasury. While a drop in the 6 trillion federal outlay bucket, it nevertheless shows how prior money printing can cause a loss of fiscal income in the future.

When a monetary authority has lost enough credibility (the money users give up a rapidly deteriorating money for precisely anything) it doesn’t much matter how one moves the small levers left under the monetary authority’s control. Hyperinflation, therefore, can be seen as a high inflation where the monetary authorities have lost control.

Bottom line:

Hyperinflations happen when the nation-state backers of a currency go out of business — as in the Balkan states and former Soviet Bloc countries in the early 1990s. They also happen from extreme mismanagement, from the Weimar Republic in the 1920s to the South American episodes in the 1980s and 1990s, or Venezuela and Zimbabwe more recently.

Remember that the German hyperinflation took place between 1922 and 1923, after wartime inflation (1914-1918) and postwar reparations debacle had gradually degraded the country’s finances and industrial capacity. Much like today’s monetary struggles, there was plenty of blame to go around but the point remains: it takes a long time for a thriving and monetary stable empire to devolve into the jaws of hyperinflationary chaos.

Every currency regime ends, gradually then suddenly. Perhaps things move faster today, but spotting a USD hyperinflation on the horizon (like Balaji did in March 2023) might be too early yet. While we might not have reached the “suddenly” part yet, we can’t be sure that the “gradually” hasn’t already begun.

America in 2023 features many of the ingredients often involved in hyperinflations: domestic turmoil, runaway fiscal deficits, a central bank unable to imbue credibility or manage its price stabilization goals, grave doubts about the banks’ solvency.

The history of hyperinflation is vast but mostly confined to the modern age of fiat. If it’s any guide for the future, a descent into hyperinflation happens much more slowly and takes a lot longer than a few months.

14 June 2023 16:36